With rapid ageing of the population in Asia, A Greater Urgency is Needed in Reforming Asian Pension Systems

- In Economics

- 12:16 AM, Jan 20, 2019

- Mukul Asher

With rapid ageing of the population, the public policy goal should be ageing with dignity. It implies that a person should be ageing-in-place, staying at home to the maximum number of years as possible, and have access to a bundle of services, especially affordable and accessible health care.

According to UN projections, the number of people over-60 years of age will increase from 205 million in 1950 to 2.1 billion by 2050.

Financial preparedness by individuals and by the society as a whole is a vital component of the overall strategy and policies for the ageing population.

Addressing financial preparedness for retirement is qualitatively a very different challenge when retirement period after institutional retirement age extends to 25 to 35 years. Increasingly many countries in Asia are also exhibiting this phenomenon.

By 2050, one in four persons above 60 years of age are projected to be in China, and one in four in India.

Yet retirement or withdrawal age from provident funds in many countries have remained at or below 60 years.

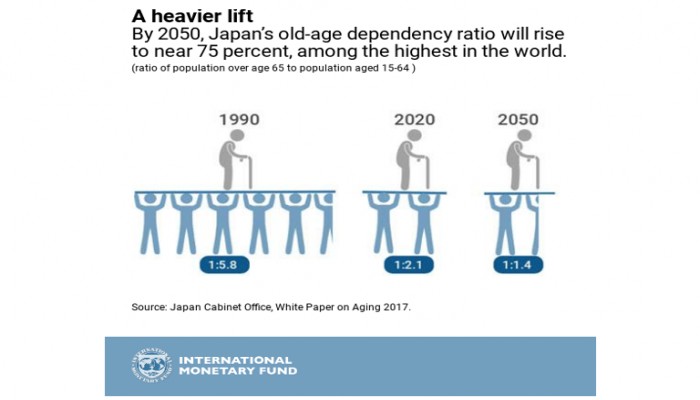

Japan has been coping with reduced number of working age persons supporting each elderly (see graph A Heavier Lift). BY 2020, only 2.1 workers will be supporting each elderly person, and this is projected to decrease to only 1.4 by 2050.

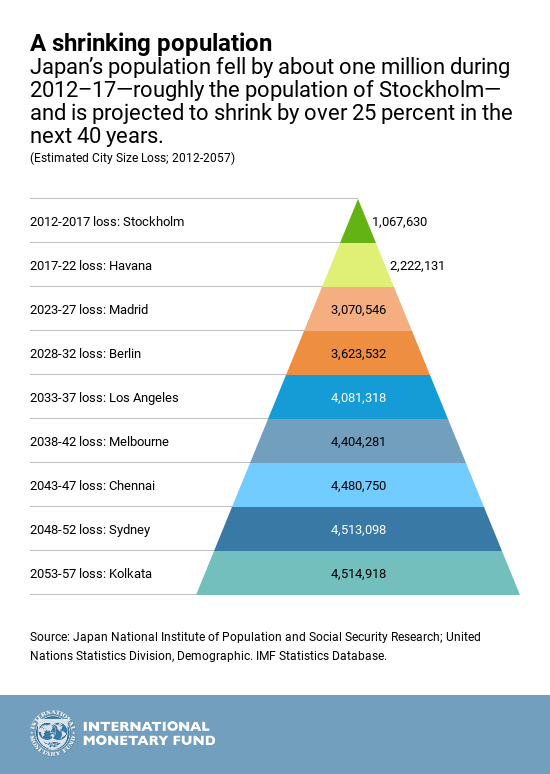

Japan is also managing with skill and dignity, absolute decline in its population (see graph on A Shrinking Population).

It is estimated that more than half of Japanese men over retirement age do paid work, and the society facilitates it. Many Asian countries will exhibit one or both of these traits of ageing in Japan, and will need to be prepared to meet the challenges.

In some countries, such as India, China, and Indonesia, intra-region variation in fertility rates and in longevity could give rise to challenges of managing internal migration.

Several recent studies have advanced the theme that new social contract or substantial reforms of existing arrangements are needed to manage challenges, including financial preparedness of ageing populations.

- One of the studies is entitled, “The New Social Contract: A Blueprint for Retirement in the Twenty-First Century” ( AEGON Centre for Longevity and Retirement (2018).The New Social Contract: a Blueprint for Retirement in the 21st Century. https://www.aegon.com/contentassets/6724d008b6e14fa1a4cedb41811f748a/retirement-readiness-survey-2018.pdf

This study is based on a survey of 16,000 workers and retirees in 15 countries, including those in Asia. The study’s context is the trends towards:

- Reduction in government retirement benefits;

- Increasing longevity and reduced fertility rates;

- Volatility in financial markets and prolonged low interest rate regimes;

- Changing labor markets with a growing role for disruptive technologies;

- The increasing importance of the digital market place.

The following findings of the study are particularly relevant:

- Nearly half of the people surveyed globally think that current retirement arrangements will make them worse of in terms of retirement income security.

- Declining physical health is the most often cited retirement concern globally. Only a fifth of those surveyed confident of health care in retirement. Many discontinue working before retirement due to own or family member’s ill health. So, healthcare should be an integral part of financial preparedness for old age.

- Only a quarter of those interviewed think they will achieve mean expected proportion of current earnings of 68% which is needed in retirement.

Asian Pension Systems: Key Characteristics and Reform Directions

There are large variations in the robustness of Asian pension systems, and in their financial, economic, organizational, institutional capacities, and in their political economies.

Nevertheless, the following broad characteristics apply to them as a whole. The reform directions are implicit in the manner which the characteristics of these pension systems have been presented.

- There has been less than adequate policy focus in Asia on financing arrangements; on developing professional provident and pension fund organizations, with appropriate governance and regulatory structures. These have resulted in high administrative and investment management costs; mis-selling of financial products; and less-than-adequate systems of coping with financial frauds which are increasingly directed at the elderly.

- The above has resulted in lower coverage of the population with access to pensions (and to healthcare); lower number of risks being addressed, and when addressed, limited benefits are provided. This means that trade-offs between the adequacy of benefits, coverage of the population, and the extent of risks that are covered must be made for any given level of resource allocation to healthcare and to pensions.

In most Asian economies, a large share of healthcare expenditure is financed out- of-pocket, with limited risk pooling, though there is some progress towards social risk pooling, particularly in India and Indonesia. Thus, the focus should be on ensuring adequacy across all three dimensions, focusing only on the number of beneficiaries or statutory coverage is not very useful.

- The main risks in retirement financing are:

- Inflation risk – the risk that the real values of retirement income decreases with the inflation rate relevant for the consumption basket of the elderly);

- Longevity risk – risk that retirement income may be inadequate in view of longer-than-anticipated lifespans;

- Survivors’ risk – risk that survivors, particularly women and children, may not be adequately provided for.

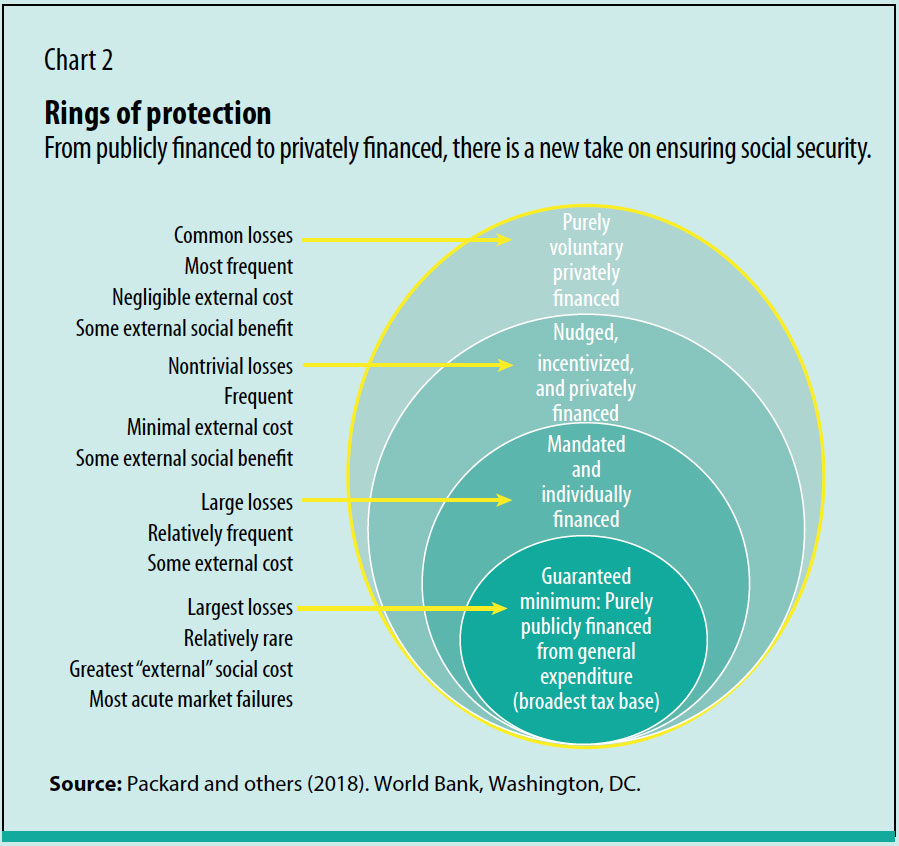

In managing these risks, sufficient social risk pooling arrangements are essential as society, rather than individuals, are better able to bear them. In many Asian countries, this aspect is inadequately recognized by policymakers.

Societies as well as households need to rely on multiple sources from which financing for retirement is derived (see chart Rings of Protection)

- The financial and capital market development has been relatively limited. This has restricted investment options by provident and pension fund organizations, and by individuals. This increases investment risk both when retirement savings and social security contributions are made during working years; and during retirement periods when macroeconomic risk and annuities market risk need to be managed.

- There is insufficient appreciation of the need to establish a strong data collection and analytical capabilities relating to pension arrangements, and to retirement behaviour. Regarding these data as a public good to be made available to various stakeholders should be accorded due priority.

Such a practice would also enhance trust in the statistical systems and in provident and pension fund organizations. These are essential to undertake needed reforms with public support.

- There is a strong case for establishing retirement behavior and pension research centers in most Asian countries, such as the Social Wellbeing Research Centre (SWRC) at University of Malaya. Such centers could address the issue of pension and healthcare policies being based on insufficient empirical evidence and policy research.

India, in particular, needs to urgently consider setting up retirement behaviour centres to enable more systematic empirical evidence-based policies on health care, pensions, and their links with labour markets, regulatory regimes, and with broader social policies. (https://www.livemint.com/Money/O5FSJGCN2sUc0OrWV6LhbL/Why-India-needs-a-centre-for-research-on-retirement-behaviou.html)

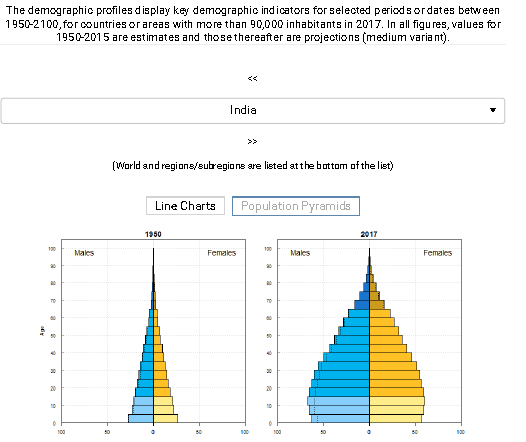

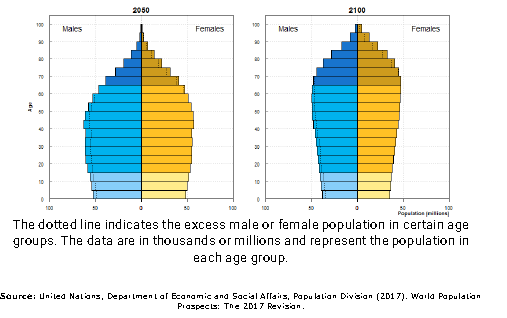

India is projected to age moderately rapidly as evidenced by the changing population profile projected since 1950 exhibited in the graph below.

7. In many Asian countries, the political economy is not conducive to long-term and sustainable pension, retirement and healthcare policies. As a result, organizational, institutional, and regulatory arrangements which are conducive to long-term savings by households with confidence are relatively weak.

8. There is relatively less emphasis in promoting financial literacy among pension and provident and pension fund trustees and staff, among policymakers, among households, and other stakeholders.

The importance of basic financial literacy has been recognized in helping to make appropriate choices for retirement income security. The consequences of poor financial choices could result in making mistakes with availing credit, spending retirement income too quickly or on inappropriate bundle of goods and services; and being defrauded by financial predators. In the U.S., most common frauds are investment frauds, and prize/lottery frauds.

In other countries, including in Asia, frauds may involve different avenues. Financial fraud however is a complex phenomenon. Increasing awareness, and raising requirements for ethical behaviour are likely to reduce the extent of the fraud.

Four of the critical financial (and economic) literacy concepts for retirement financing are the following:

- The concept of compounding interest – the value of pension savings approximately doubles when 72 divided by the rate of interest earned on savings, e.g. if interest earned is 6%, the value of pension savings doubles every (72/6 = 12) years. This implies that retirement savings should start early in the working career and preserved until retirement.

- To understand the impact of inflation on household budgets, and in the case of public funding of pensions, on government budgets. Low inflation is, therefore, of significant benefit for retirement financing.

- The concept of risk diversification where overreliance on one source of retirement finance, such as property, children, state pensions, should be avoided.

- The concept of opportunity cost: this refers to the alternatives forgone when choosing a particular retirement income avenue. Typically, undue preference for current consumption reduces opportunity for adequate retirement financing.

9. Asia has a large number of cross-border workers. They have very limited access to retirement income and healthcare benefits. Even when access is available, the costs are often prohibitive.

Concluding Remarks

- The progress towards pension reforms in Asia, leading to greater financial preparedness for old age will require all concerned pension related organizations, be it regulators, asset managers, service providers, as well as individuals and households to implement or to address the PHUI:

- Purpose of the organization – shifting from process to outcome orientation;

- Habits of stakeholders, including of officials of provident and pension fund organizations, as well as their trustees; and of individuals who will need to exhibit greater financial literacy.

- Using emerging technologies more competently and purposefully for record-keeping, lowering of administrative and compliance costs, and lowering investment management costs.

- Incentive structures for the organization, the officials, and the members to behave in a manner consistent with financial preparedness, and to enhance transparency and accountability.

Comments