The FRBM Report: Implications for the States in India

- In Economics

- 02:39 PM, Aug 09, 2017

- Mukul Asher

The first FRBM (Fiscal Responsibility and Budget Management) Act for the Union Government was enacted in 2003 under Article 292 of the Constitution (read with Article 283). Article 293 stipulates the restriction on the power of State Government to borrow.

The Union Government appointed the FRBM review Committee (Under the Chairmanship of Mr.N.K.Singh), which submitted a four Volume Report in January 2017.

As the review Committee notes, inherent in any FRBM Rules, there is a need for two sets of trade-offs. First,flexibility in implementation should be traded of against the fiscal anchor under the FRBM Rules. The second trade off concerns balancing flexibility with simplicity.

Often, flexibility in FRBM implementation adversely affects simplicity, transparency, ease of monitoring and clear communication to key domestic and global economic agents.

(http://dea.gov.in/sites/default/files/Volume%201%20FRBM%20Review%20Committee%20Report.pdfVolume-I page-37)

The Review Committee has argued that India needs to re-examine the current FRBM Rules and Fiscal Framework. The Committee suggests that medium term debt ceiling, achieved in a progressive gradual manner, be set as an anchor for fiscal policy.(http://dea.gov.in/sites/default/files/Volume%201%20FRBM%20Review%20Committee%20Report.pdfVolume-I Chapter-4)

The role of the anchor is to firmly set the goal of fiscal policy, with the government’s policies and behaviour designed to give confidence to domestic and global economic agents, so that they can base their decisions with high degree of confidence.

The Review Committee recommends combining the medium-term debt ceiling target with an operational target of fiscal policy.

The main policy recommendations of the Review Committee are stated below:

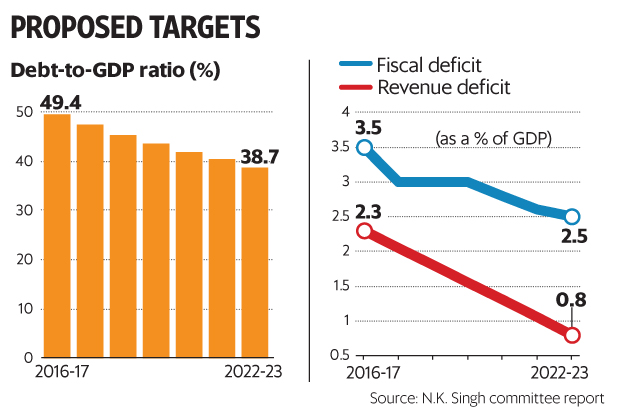

1. Adopt a prudent medium-term ceiling for general government debt of 60% of GDP, to be achieved by FY23.

2. Within the overall ceiling specified above, adopt a ceiling of 40% for the centre, and the balance 20% for the states.

3. Adopt fiscal deficit as the key operational target consistent with achieving the medium-term debt ceiling.

4. A path of fiscal deficit with fixed operational targets rather than a range.

5. A path of fiscal deficit to GDP ratio of 3.0% in FY18-FY20, 2.8% in FY21, 2.6% in FY22, and 2.5% in FY23.

6. Reduce revenue deficit to GDP ratio steadily by roughly 0.25 percentage points each year, to reach 0.8% by FY23.

Graphically, the above recommendations are summarized in Figure below.

The views of the Review Committee are consistent with the finding of the IMF that FRBM type of arrangements are more conducive to “…lower financing costs if they are accompanied by independent monitoring mechanisms”. (http://www.imf.org/en/Publications/FM/Issues/2017/04/06/fiscal-monitor-april-2017 pp.35-36)

Implications for the States

The recommendations of the FRBM Review Committee will have a significant impact on the manner in which the individual States sets the FRBM targets, and on how FRBM is implemented and monitored. The State guarantees of loans are likely to be monitored more closely. The role of an independent monitor, such as India’s CAG (Comptroller and Auditor General) is also likely to become more prominent.

The Review Committee proposes bringing State’s debt levels to 20 percent of GSDP (Gross State Domestic Product) by 2022-23; fiscal deficit to 2.5 percent of GSDP, and revenue deficit to 0.8 percent of GSDP.

These are ambitious targets, particularly as many States have incurred additional debt under the UDAY (Ujwal DISCOM Assurance Yojana ) scheme focusing on the power sector. It becomes even more imperative for the States to realize operational efficiencies envisaged under the UDAY scheme.

A report by RBI (Reserve Bank of India) on State Finances suggests that significant number of States have little or no room for debt and fiscal expansion, if they are to meet the FRBM review Committee recommendations of debt ceiling of 20 percent, gross fiscal deficit of 2.5 percent of GSDP, and revenue deficit of 0.8 percent of GSDP.

The RBI Report estimates that for the 2011-2016 period, the combined gross fiscal deficit of the states was 2.5 percent of GDP (not GSDP); but for the 2016-17 period this deficit is projected to be 3 percent of GDP. The corresponding values for the revenue deficit were 0.0 percent, and -0.1 percent of GDP. It should be noted that combined GSDP of all states is lower than the GDP of India, resulting in higher denominator. The 2016-17 estimates based on Budget Estimates which are usually over optimistic.(https://rbidocs.rbi.org.in/rdocs/Publications/PDFs/0SF2016_12051728F3E926CFFB4520A027AC753ACF469A.PDF )

The RBI Report estimates the outstanding liabilities of state government during the 2012-2017 period averaged 22.6 percent of GDP.

Moreover, the current indications are that the borrowing costs of the States are increasing. Any State perceived by the market, in an environment of growing tendency to price government debt in market determined rather than administratively determined manner, would find their fiscal choices severely constrained. This in turn will adversely impact their ability to benefit from the Cooperative (and constructively competitive federalism) initiatives.

Thus, J.P Morgan in its Asia Pacific Emerging Markets research report of 13th June 2017 finds the science of worsening state finances. It reports that even without taking into account the impact on state’s salary and pension bill of the 7th Pay Commission report, and of firm loan weavers, in some states, the state deficits have widen by almost 1 percent of GDP over the last five years.( http://7cpc.india.gov.in/pdf/sevencpcreport.pdf )

J.P.Morgan research also finds that the borrowings by the states are rising at a much faster rate than that of the Union Government. Thus, in 2013-14, market borrowing by states was equivalent to 34 percent of the Union Government’s borrowing, but by 2016-17 the equivalent share of the States was 84 percent. There are indications that market borrowing of the state could exceed that of the Union Government in the near future.

Another indicator reported is that the spreads of the state bond over the benchmark government security has tripled from thirty bps (basis points) to 90 bps in just two years. The states thus, face higher cost of rollover of their debt as well as when issuing new debt.

The higher borrowing cost has also implications for other borrowers such as the corporate sector, and therefore for the private investment levels.

The above analysis strongly suggests that the States need to accord much higher priority to improving public financial management, and in particular progressing from financing focus to outcome focus through process, systems, and human resources improvements. Better ranking in public financial management has become a critical element in competitiveness among the states in India.

Comments