Pradhan Mantri Vaya Vandana Yojana (PMVVY): A Laudable Pension Scheme

- In Economics

- 10:10 AM, Sep 23, 2020

- Mukul Asher and Vivek Singh

Pradhan Mantri Vaya Vandana Yojana (PMVVY) is a pension scheme announced by the Government of India in 2017. It is exclusively for the senior citizens aged 60 years and above.

Broad Provisions

It provides an assured minimum pension in nominal terms for ten years to those who choose to subscribe based on an assured return on the purchase price, which represents the subscription amount.

The subscriber can invest up to INR 1.5 million in the scheme. However, the limit applies only on the investing individual. Therefore, if a spouse is also older than 60 years, she or he can invest up to INR 1.5 million in the scheme separately. Thus, for a family with two senior citizens, maximum investment of INR 3 million is feasible.

If the pensioner survives till the end of the policy term of 10 years, purchase price of the annuity, along with final pension instalment is payable to the pension subscriber.

If the pensioner dies during the policy term of 10 years, the purchase price or the subscription amount is to be refunded to the beneficiary. These additional features add to the attractiveness of the scheme.

In case of emergency, the scheme permits a loan up to 75% of Principal price is allowed to be sanctioned after 3 years into the policy. The interest on this loan is recovered from pension instalments whereas the loan amount is recovered from claim proceeds

98% of Purchase price is refunded for treatment in case of medical emergencies such as critical illness of the subscriber or spouse. This enables liquidity in time of ill health episode.

The PMVVY is administered by the Life Insurance Corporation (LIC), of India which is owned by the Government. It can be purchased through LIC agents, or on-line at 1.

As of September 2020, LIC is not listed on the stock exchanges.

More than 0.1 million persons have subscribed to PMVVY 2. The scheme initially provided an assured return of 8% per annum for 10 years. The cost of differential return i.e. the difference between return generated by LIC and the assured return of 8% per annum, is borne by Government of India as subsidy on an annual basis and reimbursed to LIC.

The PMVVY has been recently modified in the following areas:

- The PMVVY, which was to end in March 2020, has been extended for three years to 31 March, 2023

- An assured rate of return of 7.4% per annum for the year 2020-21 has been provided. The interest rate will be reset every year according to market conditions. The Finance Minister to approve annual reset rate of return at the beginning of every financial year.

The minimum investment has also been revised to INR 1,56,658 for pension of INR 12,000/- per annum, and INR 1,62,162/- for getting a minimum pension amount of INR 1000/- per month under the scheme. Mode of pension payment is monthly, quarterly, half-yearly and annually based on option exercised by the subscriber. The choices are thus reflected in the price.

- Management expenses are capped at 0.5% per annum of funds of the scheme for first year of the scheme in respect of new policies issued, and thereafter 0.3% per annum for second year onwards for the next nine years.

- Exemption from GST to continue. But the annuity amount is subject to income taxation.

The expected financial liability is projected range from an estimated expenditure of INR 8290 million in the financial year 2023-24 to INR 2640 million in last FY 2032-33. The average expected financial liability for the subsidy reimbursement, calculated for annuity payment on actual basis is expected to be INR 6140 million per year for currency of the scheme. The actual interest-gap (subsidy) would however depend upon the actual experience in terms of number of new policies issued, the quantum of investment made by subscribers, actual returns generated and the basis of annuity payment 3.

PMVVY and Good Pension Design

First, by providing assured minimum return from the beginning, it enables senior citizens to plan for their retirement expenditure with assurance. LIC is a government entity, so essentially the principal and return are guaranteed. In the time of low interest rates, and volatile financial and capital markets, this is major advantage of the PMVVY.

- Moreover, even the interest rate of 7.4% is still very attractive, as 10-year central government securities yield around 6%, and 5-year fixed deposits of the bank (which are for less than 10 years and therefore carry reinvestment risk) also yield around 6% compounded.

- Second, the additional features of repayment of purchase price id subscriber survives till policy term of 10 years, and death benefit are not found in other products of similar nature.

- Third, by entrusting administration of PMVVY to LIC, with its Agent force of 11.5 million persons in 2018, enables real cost savings to the members and to the society.

- Fourth, the capping of administrative expenses to 0.5% of the total funds in the scheme in the first year, and to 0.3% in subsequent years, compares very favourably with the similar costs of between 1 and 2% for mutual funds and other financial products.

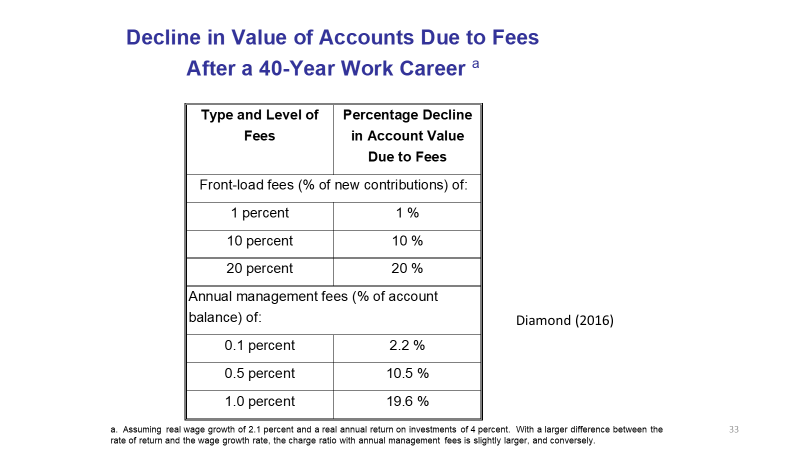

The following Table relating to pension funds and mutual funds brings out clearly why minimizing administrative costs, and investment management costs are needed for good pension design.

Table 1

Source: Diamond, P (2016), “Good Pension Design,” Presentation at National University of Singapore, 12 Jan 2016.

- Fifth, the PMVVY is designed in such a way that government’s fiscal cost is limited to the difference between the assured return, which appropriately is set each year according to market conditions, and what LIC earns, helps reduce the purchase price to the subscriber, ensures co-payment and involvement of the subscriber, and limits fiscal costs of the government. The costs for subscribers and for the government are set in a manageable manner by not being linked to inflation trends, as such linking is costly.

Providing services, such as low-cost medicines, such as Jan Arogya Yojana (of special relevance to senior citizens), housing to lower income households, and health services through Ayushman Bharat are some of the ways the government is helping households to manage expenditure.

- Sixth, it is good practice for individuals to obtain retirement income from multiple courses, including some from having skills, however basic, to earn labour market income in retirement. Age 60 is too young to retire given that an Indian at age 60 has further life expectancy of nearly 20 years, with women living longer than men. The PMVVY is designed to be one of the sources of retirement income and not the only source. This enables it to be flexible, and policymakers can experiment with other designs of pension products.

LIC should provide on its website statistics and data on PMVVY so that more detailed and rigorous data-intensive policy relevant research can be undertaken.

References

- www.licindia.in

- https://www.policyx.com/life-insurance/lic-of-india/pradhan-mantri-vaya-vandana-yojana.php Accessed on 22 September 2020

- https://pib.gov.in/PressReleasePage.aspx?PRID=1625318 Accessed on 20 September 2020.

Image Credits: The Times of India.

Disclaimer: The opinions expressed within this article are the personal opinions of the author. MyIndMakers is not responsible for the accuracy, completeness, suitability, or validity of any information on this article. All information is provided on an as-is basis. The information, facts or opinions appearing in the article do not reflect the views of MyindMakers and it does not assume any responsibility or liability for the same.

Comments