India Should Pursue Prudential Transition to Rebalancing Energy Sources

- In Economics

- 11:26 AM, Jan 04, 2024

- Mukul Asher and Vikram Sampat

Introduction

India is committed to providing a positive example in rebalancing its energy sources, with a substantial increase in the share of energy from renewable sources, while sustaining high broad-based growth. Renewable sources of energy predominantly comprise solar, hydro and wind energy. Nuclear energy is a clean energy form but it is not a renewable energy source. Together, renewables and nuclear energy form the non-fossil, clean energy.

To meet India’s increasing energy needs, an accelerated shift towards non-fossil energy sources should however, not prematurely hasten the phasing out of reliance on fossil fuels such as coal, oil and natural gas. In the recently concluded United Nations Climate Change Conference (COP28) in Dubai, there was implicit consensus that fossil fuels will continue to play some role in global energy sources for some time to come.

India’s imperative for balancing energy sources

By the end of Amrit Kaal - 2047, if not sooner, India is set to emerge as the third largest global economy. Reliable projections state that India’s GDP will be USD 5 trillion by 2027-28, USD 10 trillion by 2035 and reach a GDP of USD 26 trillion by 2047. India has been the fastest growing large democratic country for several years and the consensus is that this is likely to continue for some more period.

The primary growth enablers for India are identified by Earnst and Tong in a recent report1 India @100 as:

- India is the world’s information technology hub driving continued strong growth in services exports. Whose significance in global trade is increasing

- Digitalization of India with 1.2 billion telecom users and 837 million internet users along with the Government’s thrust on building digital public infrastructure and its widespread adoption provides a unique competitive advantage to India to drive growth in innovation and entrepreneurship;

- Filling of the credit gap through the digital economy;

- Start-up India sector is thriving on private capital;

- Infrastructure growth making domestic manufacturing more competitive and adding to future growth prospects;

- India will continue to have a relatively young population compared to its competitors such as China and

- Policy focus on making India’s energy supply more sustainable

There is a positive relationship between growth in GDP and per capita income with accompanying structural changes such as a higher share of manufacturing in GDP on the one hand and growing energy demand on the other. As data in Table 1 indicates, India’s primary energy consumption per capita is only about a third of the global average, but as India’s GDP increases, this ratio is likely to increase.

Table 1: Primary energy: Consumption per capita

|

Gigajoule per capita |

2021 |

|

US |

279.9 |

|

Total North America |

227.0 |

|

Total Europe |

122.0 |

|

Total CIS |

163.0 |

|

Total Africa |

14.6 |

|

China |

109.1 |

|

India |

25.4 |

|

Total Asia Pacific |

63.6 |

|

Total World |

75.6 |

|

of which: OECD |

167.9 |

|

Non-OECD |

56.2 |

|

European Union # |

135.0 |

Source: BP Statistical Review of World Energy, 2022, accessed on 31st Dec, 2023

While Indian per capita energy consumption (at 25 Gigajoules/capita in 2021), is relatively low in comparison with other large economies globally, India’s total energy consumption (at 927 MTOE - Million tons of Oil Equivalent - for the year 2021) is the third largest in the world according to World Energy & Climate Statistics – Yearbook, published by Enerdata2

Overall, Indian energy consumption is set to rise at a CAGR (Compound Average Growth Rate) of 1.9%, the fastest among the large global economies, according to ExxonMobil's Outlook for World Energy (published in January 2023, accessed on May 15, 2023), which projects India's overall energy consumption to grow from 38 to 66 quadrillion BTU between 2021 and 2050 with India's share of energy consumption in the world growing from 6.9% to 10.0% in the same period.

This has important geo-political ramifications in terms of pressures on India to become a constructive and innovative partner in addressing climate change. The key objective for India should be to improve the energy intensity (EI) of GDP measured as the Energy consumption of the country (in kilo oil equivalent divided by the GDP of the country expressed in dollars at the constant exchange rate, price and purchasing power parities of the year 2015, koe/$15p).

In 2021, India’s Energy intensity (EI) was 0.100, about the same as for Brazil, but higher than for the OECD (0.089). India needs to improve its EI, even as it increases its share of manufacturing, by more efficient and innovative use of a mix of energy sources. If it succeeds in doing so, it will enhance its international competitiveness in comparison to countries such as Indonesia, China and Brazil.

India’s record of energy intensity improvement has hitherto been impressive. India is following the global trends in reducing the energy intensity (EI) of its GDP growth (As against the global EI of GDP improvement of 1.8% per year, Improvement in India has been 2.2% per year from 2010 to 2021). (Source: Statistical Yearbook 2022 of Enerdata, a global energy consultancy. Accessed on May 15, 2023 – Enerdata.net )

India’s approach to rebalancing its energy mix

India is one of the few large countries not endowed with large fossil fuel reserves (Oil and gas reserves constitute 0.3% and 0.7% respectively of global reserves, aside from coal which is 10.3% of global reserves, leaving it open to oil and gas producers around the world for its energy needs. (Source: BP Statistical review of World energy 2022, accessed on May 15, 2023)

Energy management also has important implications for India’s external sector management. Of the total merchandise import bill in India of USD 710 billion in FY ‘23, 37% or USD 260 billion was accounted for by energy imports, according to the official data from the Reserve Bank of India (RBI). This contributed to almost the entire trade deficit of India amounting to almost 3 percent of GDP. Therefore, sound macro-economic management is an integral part of India’s prudential management of energy sources.

A major goal of India’s Atmanirbhar initiative is the relative reduction of imported energy expenditure as a % of GDP. Prime Minister Modi's commitment to Atmanirbhar Bharat aims to make India energy independent by 2047. However, India currently imports 90% of its oil and 80% of industrial coal. So, energy independence must be interpreted to mean acquiring enough capabilities and resources to be resilient against any energy shocks and not being excessively dependent on one source of energy or on one energy producer in the whole energy value chain.

The government of India has set aggressive targets for growth in renewable energy capacity. India is the world's fourth largest consumer of electricity and the world's third largest renewable energy producer with 40% of energy capacity installed in the year 2022. Ernst & Young's (EY) 2021 Renewable Energy Country Attractiveness Index (RECAI) ranked India third behind the USA and China3.

Currently, (July 2023) India has a power generation capacity of 424 GW out of which combined non-fossil fuel power capacity is 177 GW or 42%, and 88 GW more non-fossil energy projects are under execution. Under India’s Panchamrit Climate Action Plan (CAP), the government has set a target of expanding the non-fossil fuel energy capacity to 500 GW by 2030. India ranks fourth globally for total renewable power generation capacity additions.

This capacity is expected to fulfil at least 50% of India’s fast growing energy demand, help reduce India’s carbon intensity of GDP below 45%, reduce carbon emissions by 1 billion tons by 2030 and pave the way for achieving India’s Net-Zero emission target by 2070 4,5,6.

Indian private sector is investing at a significant scale in the green energy sector

India’s energy transition and transformation is being executed through public-private partnership (PPP). The private sector has seen opportunities in being a constructive partner in India’s energy transformation. Prominent among the private sector companies are Tata Power, Adani Green Energy, Reliance Industries (New Energy), JSW Energy, Sterling and Wilson, Inox Wind, Indian Oil, ONGC, GAIL and Borosil Renewables.

Illustratively, Reliance Industries (New Energy) plans 4 giga- factories with multi-billion USD investments for solar PV, storage batteries, hydrogen electrolyzes and hydrogen fuel cells with a vision to transform the renewable energy landscape of India, and gradually of other countries.

Reliance Industries (New Energy) has announced a wave of partnerships with REC, NexWafe, Sterling and Wilson, Stiesal, and Ambri for an estimated cost of USD 1.2 billion. With these investments, this company has acquired the expertise and technology portfolio to start to build a fully integrated end-to-end renewable energy ecosystem through solar, batteries, and hydrogen. The company is targeting solar manufacturing of 100 GW and green hydrogen costs of USD 1 per kg by 2030. It will spend USD10 bn in these businesses over the next three years to meet these targets7.

Key economic aspects of renewable energy in India

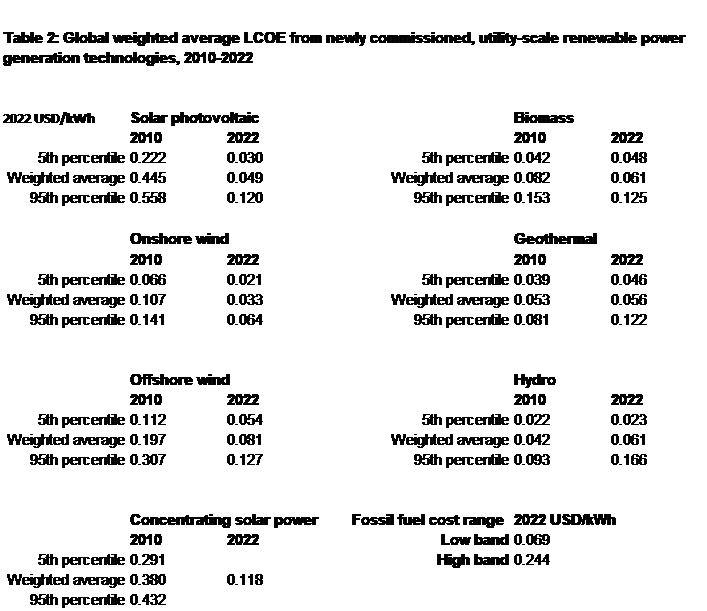

According to the International Renewable Energy Agency (IRENA), the costs of renewable power generation are increasingly competitive in comparison to fossil fuel-based power sources. Specifically, the weighted average LCOE (Levelized cost of energy) for solar power in 2022 at USD 0.049/Kwh is almost at 10% of its cost in 2010. (Indian utility scale solar power at $0.0374/Kwh is globally very competitive). LCOE of onshore wind is $0.033/Kwh and compares favourably to the low band of fossil fuel cost at $0.069/Kwh. (Table 2)8.

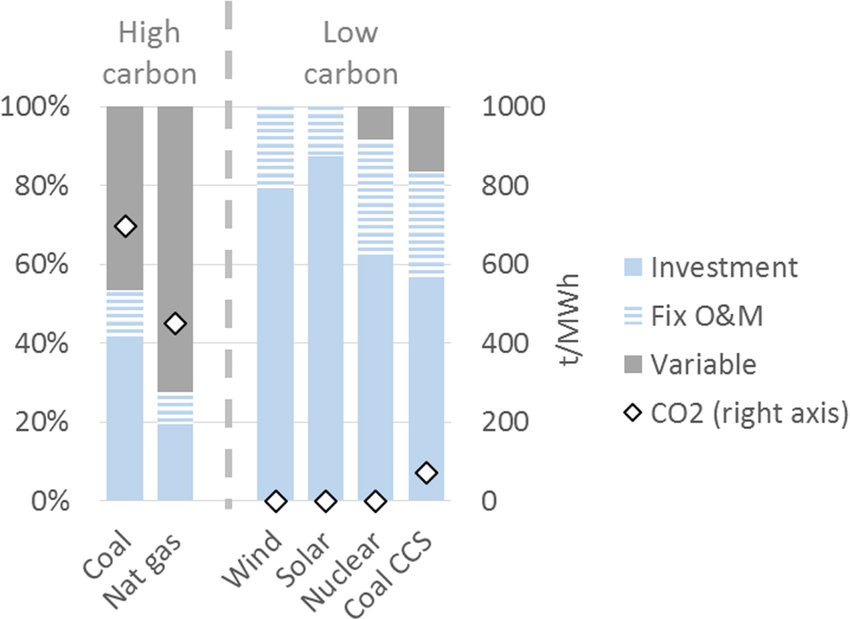

Renewable power is made all the more attractive due to their negligible variable costs of generation. This means once the capacities are set-up, the energy is generated at little or no additional variable cost. (Figure 2). This will make India highly competitive in the manufacturing and services sectors. Widespread adoption of renewable energy in India will create a business ecosystem in India, akin to that in the USA which had an indigenous oil supply and which allowed rapid economic progress without the macro-economic strains imposed by large energy import bills9.

Figure 2: Cost composition of different power generation technologies

A Vision for leap-frogging Indian economy through non-fossil energy

Indian climate and topography are suited for large-scale renewable energy adoption, in particular, solar and onshore wind energy, where Indian LCOE is very competitive against global peers and also with fossil fuel alternatives.

India’s still nascent and expanding electricity grid will allow the adoption of sophisticated, state-of-the-art electronics to seamlessly integrate clean energy into the grid (which has been a major challenge with older technology-based developed market grids trying to integrate with renewable energy) along with low-cost intermediate power storage to stabilize the intermittent generation of renewable power.

Such power storage will move away from scarce, high-cost Lithium batteries to other abundant, low-cost metals like sodium through a strong push in technological advancement. Indian energy corporates are aggressively pursuing cutting-edge technologies for batteries and renewables.

The future vision for India envisages a negligible variable cost non-fossil energy forming a large proportion of total power, the backbone which supports rapid economic transformation. This power will flow through the modern, electronically controlled grid supported by balancing battery capacity.

The industrial fuel will be supplied predominantly by green hydrogen, which can be generated near the consumption points by the hydrogen ecosystem of electrolysers and fuel cells or green methanol generated in mega methanol plants.

Personal mobility will be largely supported by electric vehicles running on green power. India is set to emerge as the largest and most affordable EV market and manufacturing hub globally. This will revolutionize India’s mobility with an aim to also eliminate dependence on scarce metals for batteries. Here again, the growing car population will allow India to create an EV charging infrastructure with more ease compared to the developed world which will need to retrofit EV charging in the existing fuel station infrastructure. Indian domestic and external policies would however need to ensure that critical metals and minerals needed are managed sustainably.

India also has a massive opportunity to devise innovative solutions to power its smaller villages and towns, with low power demand, through a combination of local solar power and intermediate storage, without the need for grid integration.

An energy independent India will not only be fully sustainable but will also emerge as a very competitive manufacturing and services economy globally and help sustain high but broad-based growth to progress towards India’s Amrit Kaal vision of emerging as a developed nation.

References

- https://www.ey.com/en_in/india-at-100#:~:text=Realizing%20the%20potential%20of%20a%20US%2426%20trillion%20economy&text=The%20Government%20of%20India%20has,6th%20of%20the%20global%20population (accessed on Dec 31, 2023)

- www.enerdata.net (Accessed on May 15, 2023)

- https://en.wikipedia.org/wiki/Renewable_energy_in_India (Accessed on 24th Dec 2023)

- https://economictimes.indiatimes.com/industry/renewables/india-to-achieve-500-gw-renewables-target-before-2030-deadline-rk-singh/articleshow/103936965.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst (Accessed on 24th December 2023)

- https://pib.gov.in/PressReleaseIframePage.aspx?PRID=1961797#:~:text=Dr%20Jitendra%20Singh%20said%2C%20India,1%20billion%20tons%20by%202030%3B (Accessed on 24th December 2023)

- https://www.investindia.gov.in/sector/renewable-energy#:~:text=This%20is%20the%20world's%20largest,(as%20of%20July%202023). (Accessed on 24th December 2023)

- https://www.livemint.com/industry/energy/6-indian-companies-betting-big-on-renewable-energy-11638961823514.html (Accessed on 24 December 2023).

- https://irena.sharepoint.com/:x:/s/statistics-public/Eb5hlLV542tFjM5UpkCAo6wBcKB-MdcusRt7KryLhrC9rA?rtime=2I-Hh_IJ3Eg (Accessed on 31 December, 2023).

- https://www.researchgate.net/figure/Cost-composition-of-different-power-generation-technologies-Typical-parameters-were_fig1_309751374 (accessed on January 1, 2024)

Image source: ScienceDirect.com

Comments